Probability and Random Processes

Descriptive Statistics

Statistics

Statistics are the summarization of a set of data that has been collected, which demonstrates random variation. Extracting meaning from data.

Inferential Statistics

Inferential Statistics make inferences about a situation based on data, such as forecasting. Descriptive statistics can be the basis for inferences.

Representative Values

- Mean - The sum of all numbers in a list divided by the number of items in the list

- Median - The middle value in a list ordered from smallest to largest

- Mode - The most frequently occuring value in a list

- Range - [Min, Max]

- Variance - Average of deviation from the mean squared

- Standard Deviation - Measure of average absolute deviation

- Skewness - Measure of the shape of the distribution function

- Quantiles - Generalization of the median to percentiles

Observational vs. Experimental Data

Experimental Data involves manipulating objects to determine cause and effect in data. Observational Data refers to data extrapolated from naturally occurring events.

Basic Probability

Probability Calculus

Probability events have a total probability between zero and one.

An event that is sure to happen

The definition of probability for how often an event is observed can be related to the number of repetions of the experiment.

Counting the probability of heads in a set of coin tosses

The larger the number of repetiions, the higher accuracy with which we can predict the likelihood of an event happening.

Probability Model

Events

Events are elements in the set of possible outcomes in an experiment.

Sample Space

The set of all possible outcomes for an experiment.

The sample space for a dice roll

Subsets containing events in the sample space

The complement of a subset

Event Algebra

Or

The combination of two or more sets.

For

And

The set of events which occur in two or more sets.

For

- Mutual exclusion:

- Inclusion:

- Double complement:

- Commutation:

- Associativity:

- Distributivity:

- DeMorgan’s Law:

Probability of Events

- For any event

: - For the full set,

- If

and are Mutually Exclusive then - Axiom 3 can be extended:

Mutual Exclusivity refers to the fact that

Non-Mutually Exclusive

In cases where

This is due to the fact that in overlapping events, the same area of probability will be counted twice, though it has no statistical importance.

Non mutually exclusive OR

Complement of an Event

From expanding on these axioms, it can be seen that the complement of an event has a probability related to subtraction of itself from the sample space probability. If the chance of the event happening is known, the chance of an event not happening is found by subtracting this from absolute certainty.

The complement of a set versus the whole

Statistical Independence

Two events

Statistical independence

This refers to the fact that statistical data will happen independent of the preceding events. If you flip a coin, the probability of the next coin will be the same. If you take items from a bin, the probability of the next item being picked will go up, and is therefore dependent.

Repeated Independant Trials

From the rule of statistical independence, we can process repeated trials.

Coin Flips

Knowing that the probability of either event is 0.5, we can take the list of possible outcomes and calculate the probability.

Sampling with Replacement

In this case, we consider an event where an event occurring does not subtract from a finite amount of events, ie a coin flip. In the case of heads or tails, there aren't one less heads or tails. So it is as if we replace the event in our sample space.

Sampling without Replacement

Finite amounts of events that can be subtracted from the whole. If this event happens, it won't happen again, as if we have taken our card from a deck of cards and not placed it back in the deck.

Order of Outcomes When Sampling Without Replacement

Cases when its important what order events occur in. Did we draw the Ace of Spades within the first 3 draws? The number of each event is not important.

K-Tuples

When a trial is repeated

The Rule of Product

How many possibilities are there for the formation of

The Rule of Product

By this rule, the number of possibilities when rolling a dice, then flipping a coin, will be

Permutations of Unordered Outcomes

We no longer care in what order outcomes occur, we are only concerned with the number of outcomes of a certain sort across all trials.

This involves the number of ways we can choose

Permutations Without Replacement

- Experiments with two or more possible outcomes

- These trials can be repeated independently for

times - For each

th trial the outcome from the previous is removed - Probabilities change for each consecutive trial

The resulting set is ordered, but as mentioned before, we only care about the number of possible permutations from these elements.

The number of possible sets is

Example - The 13 cards of a suit in a deck of cards can be laid out in

If you want just

Consider this problem - Lisa has 13 different ornaments and wants to put 4 ornaments on her mantle. In how many ways is this possible?

Using the product rule, Lisa has 13 choices for which ornament to put in the first position, 12 for the second position, 11 for the third position, and 10 for the fourth position. So the total number of choices she has is

From this example, we can see that if we have

The notation for permutations is

Combinations of Non-Unique Outcomes

A combination is a way of choosing elements from a set in which order does not matter.

Consider the following example: Lisa has 13 different ornaments and she wants to give 3 ornaments to her mom as a birthday gift (the order of the gifts does not matter). How many ways can she do this?

We can think of Lisa giving her mom a first ornament, a second ornament, a third ornament, etc. This can be done in

There are

Rule of Combinations or Unordered Permutations

The notation for combinations is

Conditional Probability

A conditional probability is a probability that a certain event will occur given some knowledge about the outcome or some other event.

Rule of Conditional Probability

A simple example - A fair 12-sided die is rolled. What is the probability that the roll is a 3 given that the roll is odd?

This is

Because

Conditional Probability if statiscally independent

Bayes Theorem

When attempting to compute the conditional probability of two events, when only one event is known, the Bayes Theorem allows for a workaround.

Consider

Bayes Theorem

We can expand the equation in the numerator to demonstrate fully:

Therefore,

Total Probability

If

Total Probability

Knowing this,

Bayes General Rule

Total Probability, when $A_1$, $A_2$, $A_3$ form a partition

Random Variables

Random variables deal with a function

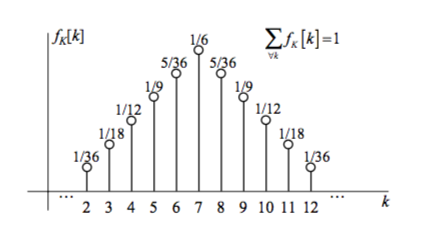

Discrete Probabilty Distributions

Discrete random variables involve events with a discrete set of values.

Probability Mass Function

The Probability Mass Function, or PMF

For a given value

Consider

Bernouli Random Variable

A Bernoulli RV is a discrete variable which will only produce values of

Binomial Random Variable

The Bernoulli concept can be extended with combinatorics, for example in the base of binary transmission error. When detecting the error in the first

As shown in earlier sections, there are

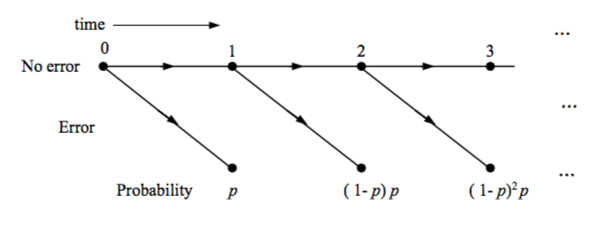

Geometric Random Variable

Geometric RVs concern a wait for an event to happen. Should the expected event be given

Geometric Random Variable PMF (0 $\leq$ k $<$ $\infty$)

Poisson Random Variable

For a situtation where revents occur randomly at a given rate

Poisson Random Variable PMF

Note that for finding the probability of an event occurring after time

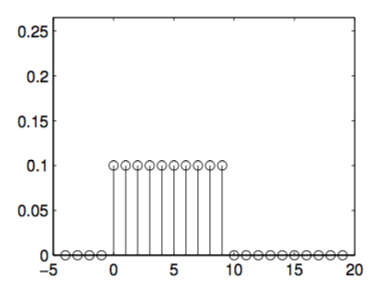

Uniform Random Variable

When all events are equally likely, the probability of each can be found easily from the uniform random variable PMF.

Uniform Distribution

Continous RVs and Their Distributions

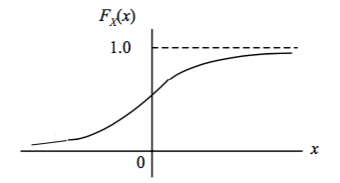

For values which can take on a continuum of values, such as voltage, velocity, and mass, new tools are used to analyze their probability. The probability of these events is determined using the Cumulative Distribution Function or CDF, which is written as

By this notation we can see that by following the graph from left to right, the probability of the event occuring to the left of value

When finding the probability of a value occurring between points

CDF Probability Within a Range (b $>$ a)

The Probability Density Function or PDF is a derivative of the CDF that can also be used to find this probability:

CDF Probability Within a Range (b $>$ a) From Integration

This can be seen to be similar to the Probability Mass Function, as it will integrate over its full range to

To use the PDF to find the probability of a number

PDF Probability Within a Range ($a < a + \Delta x$)

Integrating over a range (

Common Continuous RVs

Exponential Random Value

An extension of the Geometric Random Variable to the continuous realm, this represents a continuous graph of wait times where again

Its PDF follows

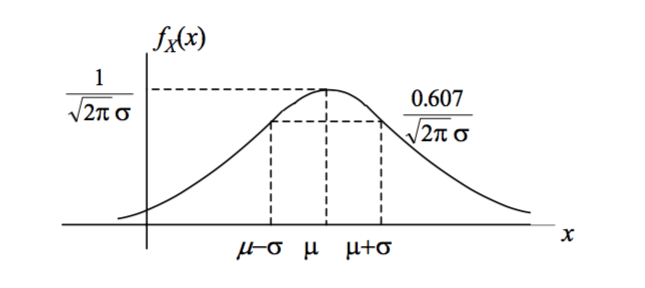

Gaussian RV

The Gaussian or "normal" random variable arises naturally in numerous cases. It can be defined by its mean,

The Gaussian PDF

The square of the standard deviation,

The standard form of the PDF, centered at

The Standard Gaussian Function

And as with any other CDF,

These

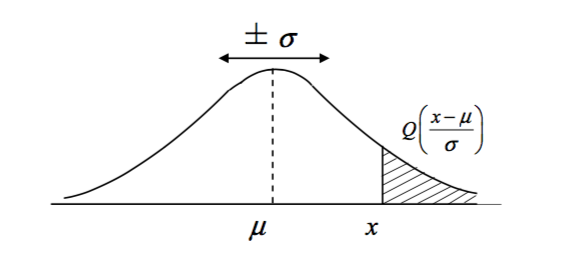

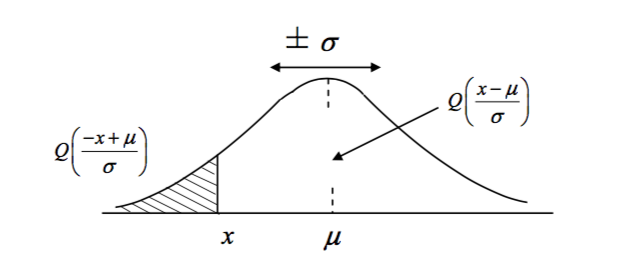

Gaussian Q Values

In cases where the probablity of values at either tail of a Gaussian is required, such as

The Gaussian Q Function

When a value

The Gaussian Q Function

The Gaussian Q Function with Negative Argument

Expectation

Expecation can be considered the average of the expected values in a sample space, where the values are weighted by their probability and summed.

Expectation of a Discrete RV

For continuous random variables, when the PDF exists, the expectation can be calculated whenever the variable converges absolutely:

Expectation of a Continuous RV

An important feature of the expectation is its invariance.

Moments

The moment is the produced when the

Continous Moment

Discrete Moment

The first moment is the mean, and each further

Central Moments

The Central Moment is a mean of a random variable not centered at 0. Of particular importance is the variance, the square root of which will grant the width of the distribution.

The 2nd Central Moment

The mean of $X$

The Standard Deviation is represented as

Also note,

Entropy

From the topic of information encoding, it was found that the definition of information for an event

And the average of information for two exclusive events

The definition of average information is in fact an expectation for two events that form a partition of a sample space.

For a partition

or,

Multiple Random Variables

Discrete Random Variables

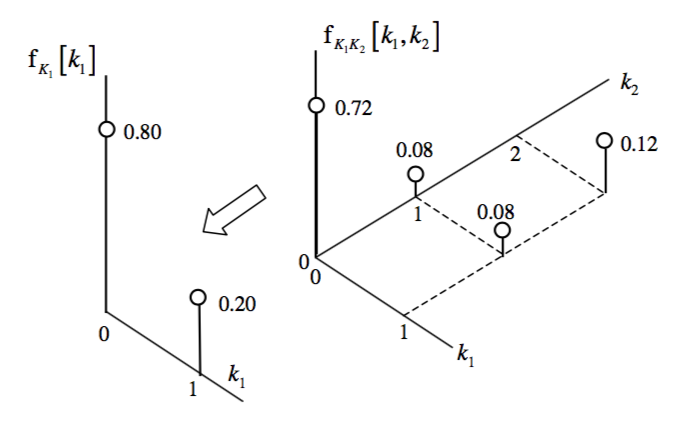

The Joint PMF

Joint probability distribution can be thought of as

Or as

A relationship can be deterministic, such as

Joint Probabilities refers to the probability of two variables taken together, such as

Recall from single random variable discussion, the PDF is the derivative of the CDF. Therefore, for cases where there are multiple variables:

For continuous distributions, the variables

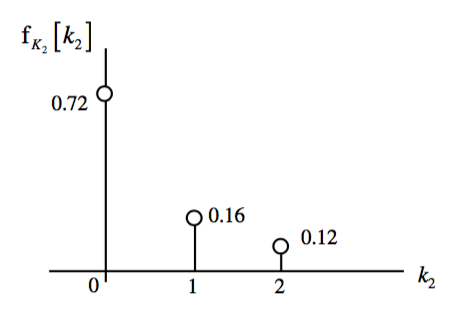

From each joint distribution, individual distributions for each variable, or \textbf{Marginal Distributions} can be found. These are simply the PDFs of the individual random variables found in earlier sections.

Independant Random Variables

From earlier in the course, events were defined as independent if

Notice that this is a special condition for random variables and does not apply in general! In particular, if two random variables are not independent, there is no way that the joint PMF can be inferred from the marginals. In that case the marginals are insufficient to describe any joint properties between

Continuous Random Variables

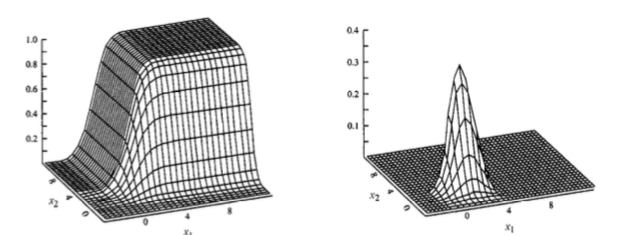

Joint Distributions

CDF:

PDF:

Joint continuity can be proven if the PDF evaluates to 1.

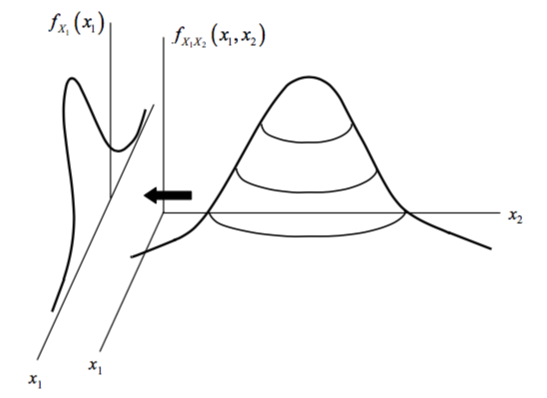

Marginal PDFs

Similar to the marginal PMF, each distribution

Correlation

Correlation is defined as the similarity between two random variables

The correlation is calculated using the expectation, worked out as the expectation for

The correlation can be misleading if both

Where

Note - Covariance is similar to variance, in that variance is a measure of how to the outcome of

Also similarly to variance:

Correlation Coefficient

If comparing the correlation of one of pair of random variables to the correlation of another pair of random variables, both can be normalized based on their standar deviations:

Where

Invariance of Expectation

If a random variable

Then moments for

Sum of Multiple RVs

Because the expectation

Therefore, because variance will distribute via multiplication:

PDF for

Begin by finding the CDF in a method similar to discrete RVs:

Note the limit of integration for the

The PDF can be obtained from this because

Because

If the two RVs are independent,

Notes on Sums of Independent RVs

- When

and are independent, = 0 and = + , while - If

and have the same distribution,

Sums of Dependent RVs

In the case of

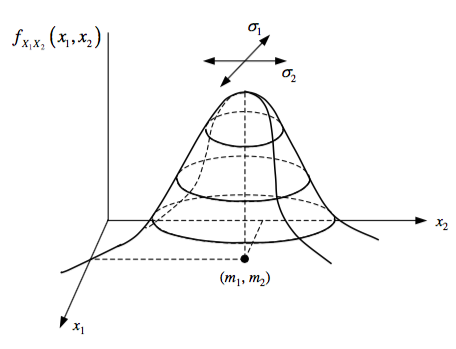

Bivariate Gaussian

Two joint RVs with Gaussian characteristics together will have a joint Gaussian characteristic, called bivariate or multi-variate for more than 2.

Limit Theorems

In other terms, when the number of trials approach large numbers, the mean of the trials will be